Why consumers still don't fully trust the platforms they buy from, and what that means for brand budgets.

US social commerce passed $100 billion in gross merchandise value (GMV) in 2026, the total value of goods sold through social platforms, up roughly eighteen percent in a year. By most accounts, it is the defining growth story of US digital retail in the 2020s. TikTok Shop drives the single largest share of that spend, and Instagram, YouTube Shopping, and Pinterest are all pushing deeper into in-app checkout. The infrastructure is there. The creator ecosystem is there. The supply chain integrations are there.

One thing is not: consumer trust.

In our research, an independent survey of 1,000 US adults who made at least one social media purchase in the past six months, shoppers told us, unprompted, that trust matters about three times more than lower prices when they decide where to buy. Not price. Trust.

That gap is not a rounding error. It is the central tension of social commerce in 2026.

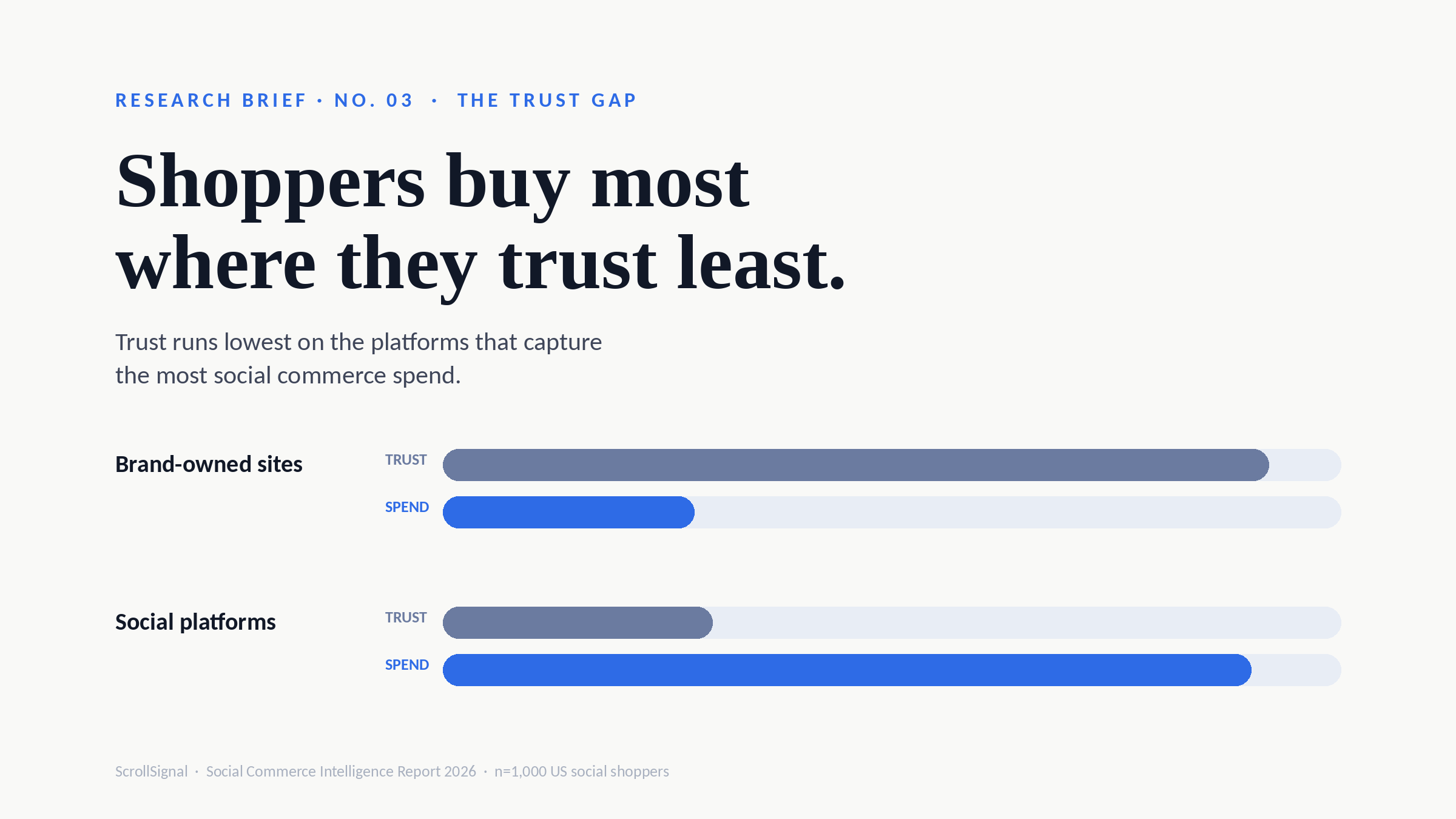

Here is the part that makes it a paradox rather than a warning. Shoppers are not staying away. They are spending heavily on TikTok and Instagram, the exact platforms they tell us they trust least. Low trust and high spend are happening at the same time, in the same people. The gap does not stop the purchase. It shapes everything around it: what closes, what gets returned, what gets bought again, and where the next purchase actually happens.

What the research actually found.

We also asked how much shoppers trust the major places they buy: brand-owned websites and each social platform, across product authenticity, post-purchase support, and data handling.

The pattern was consistent:

- Brand-owned websites lead on trust. The strongest social platform sits well below them.

- Every social commerce platform clusters lower, with meaningful gaps between the best and worst performers in the social set.

- The gap is widest on post-purchase support and data handling, the things that matter most after a transaction, and where social platforms have historically invested least.

Demographic patterns underneath that headline are where the story gets interesting. Women, who drive the majority of social commerce spend, report lower trust in social platforms than men, even as they spend more on platforms like TikTok Shop. Shoppers aged 18 to 24 report the lowest satisfaction with social commerce and the highest negative experience rates, despite being the cohort most exposed to it. Household income above $150K correlates with dramatically higher trust and engagement, suggesting the affluent buyer opportunity in social commerce is real but narrow.

Why this matters for brand budgets.

The trust gap is not a theoretical concern. It is a practical problem for any brand allocating media investment across channels.

Consider what consumer trust actually controls:

Cart abandonment. Lower trust means more second-guessing between Add to Cart and Checkout. In social commerce, where the decision window is measured in seconds, even small trust deficits compound into real revenue loss.

Post-purchase experience. Trust shapes whether buyers return, recommend, and forgive mistakes. On a platform shoppers do not fully trust, one bad experience becomes terminal.

Price elasticity. The categories where social commerce performs best, beauty, apparel, impulse lifestyle, are exactly the categories where trust premiums are most easily converted into willingness to pay. Losing trust means losing pricing power.

Attribution. If a shopper discovers a product on TikTok but closes the app and buys it from Amazon instead, did TikTok do its job? For most brands measuring ROI inside the platform, the answer is "no, we don't see that click." But commercially, yes, the discovery worked. The trust gap is partly why social commerce ROI looks worse in platform dashboards than it probably is.

What to do about it.

Three implications stand out.

First, rebalance the budget mix based on trust, not just reach. A platform with high reach and low trust is a discovery channel, not a closing channel. Plan and measure it accordingly.

Second, do not outsource trust to the platform. The brands that perform best on social commerce in our research are the ones that show up with consistent visual identity, transparent return policies, and genuine creator relationships, not the ones that simply buy the most in-app ad inventory. Trust is built at the brand level. Platforms are infrastructure.

Third, measure across the funnel, not inside one platform. If your social commerce reporting ends at "clicks in-app," you are measuring roughly one-third of the activity your creator content is actually generating. The rest is clicking out to Amazon, to your website, to Google, and back around. More on this in our next brief.

The full data, including platform-by-platform trust rankings, cross-tabs by age, gender, income, and education, and the category-vs-platform matrix, is in the Social Commerce Intelligence Report 2026. The free executive summary covers the headline findings. The full report (PDF) is available at three license tiers.

ScrollSignal is an independent B2B research firm publishing original consumer research on social commerce. No platform funding. No sponsored findings. Just the data.