The standard story about a purchase has a shape. A consumer sees something. They consider it. They compare alternatives. They wait, sometimes hours, sometimes weeks. Then eventually they buy.

That's not what's happening on social. The shape is shifting.

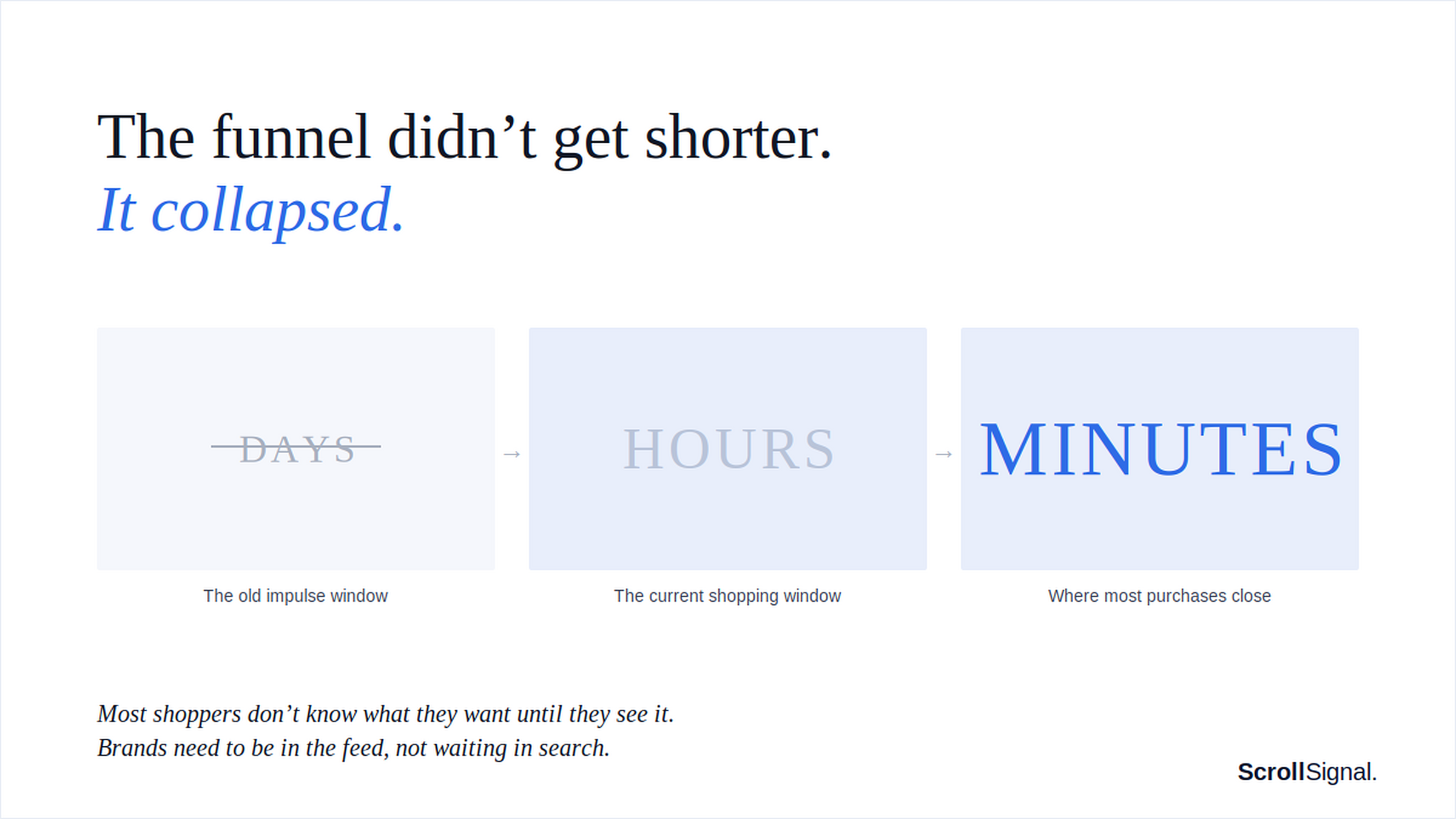

73% of the social commerce purchases reported by our 1,000-person panel were unplanned. The product wasn't on anyone's list when the day started. They saw it and they bought it. Most of those purchases closed within hours of first exposure, not days.

The consideration phase that so many brands built their retargeting cadences around is disappearing. Discovery and purchase have collapsed into the same social moment.

But here's the part I keep coming back to: consumers are doing this on platforms they don't even fully trust. Every social platform sits well below brand websites on trust attributes in our data. Speed overrides caution at checkout. That's the speed-trust paradox.

Why this breaks the standard playbook.

The traditional purchase funnel — the journey from awareness to consideration to conversion — assumes time. Days, sometimes weeks. Retargeting windows are built on those timeline assumptions. Email automation cadences inherit them. So does most attribution modeling.

If purchase happens within hours of first exposure, the consideration phase has either compressed dramatically or combined with discovery.

The implications converge regardless.

If your retargeting window opens 24 hours after the first product impression and the bulk of purchases are completed inside that window, much of your retargeting is chasing purchases that have already occurred.

If your "we saw you looking at this product" email lands 48 hours later, you're catching the long tail of a short curve, post-conversion.

If your inventory and customer service teams are staffed for a multi-day rollout, a creator drop or a viral product moment might overwhelm them on Day 1 and disappoint everyone on Day 2.

The full report breaks down how the impulse window varies by age cohort, by platform, and by category — and what the trust-share gap actually looks like across each social platform.

Read the free executive summary for the highlights, or the full report for the cross-tabs and strategic implications.

How we did the research.

ScrollSignal surveyed 1,000 US shoppers aged 18–64 who made a purchase on TikTok, Instagram, Facebook, YouTube, or Pinterest in the past six months. More than half of all panel members screened did not qualify, so every finding reflects active social commerce shoppers, not casual browsers.

The study was fielded in April 2026 via an independent consumer research panel and stratified to US Census on age, gender, and region. All figures reported at the stratified level.